Arun Gandhi “Mr. Carmack, What you have shown in the scenario is what we are constantly doing at the personal level as well as the public level. It is the policy of exploitation that the rich employ against the poor. This is why grandfather [Mahatma Gandhi] said ‘Materialism and morality have an inverse relationship – when one increases the other decreases.’ If I may, I would like to keep the videos as resource material to teach students about economic violence in the world. With good wishes. Yours sincerely, Arun Gandhi, M.K. Gandhi Institute for Nonviolence”

Arun Gandhi “Mr. Carmack, What you have shown in the scenario is what we are constantly doing at the personal level as well as the public level. It is the policy of exploitation that the rich employ against the poor. This is why grandfather [Mahatma Gandhi] said ‘Materialism and morality have an inverse relationship – when one increases the other decreases.’ If I may, I would like to keep the videos as resource material to teach students about economic violence in the world. With good wishes. Yours sincerely, Arun Gandhi, M.K. Gandhi Institute for Nonviolence” Milton Friedman “Mr. Carmack, As you know, I am entirely sympathetic with the objectives of your Monetary Reform Act…You deserve a great deal of credit for carrying through so thoroughly on your own conception…I am impressed by your persistence and attention to detail in your successive revisions… Best wishes. Milton Friedman,” Nobel Laureate in Economics; Senior Fellow, Hoover Institution on War, Revolution and Peace

Milton Friedman “Mr. Carmack, As you know, I am entirely sympathetic with the objectives of your Monetary Reform Act…You deserve a great deal of credit for carrying through so thoroughly on your own conception…I am impressed by your persistence and attention to detail in your successive revisions… Best wishes. Milton Friedman,” Nobel Laureate in Economics; Senior Fellow, Hoover Institution on War, Revolution and Peace

Malachi Martin “I endorse the video because people should know what is happening.” – Malachi Martin, late Professor at the Pontifical Biblical Institute and a close associate of Pope John XXIII; author of: The Windswept House; Vatican; The Keys of the Blood, and numerous other books

Malachi Martin “I endorse the video because people should know what is happening.” – Malachi Martin, late Professor at the Pontifical Biblical Institute and a close associate of Pope John XXIII; author of: The Windswept House; Vatican; The Keys of the Blood, and numerous other books Russo “I’m a big fan of The Money Masters. It’s undoubtedly the best work on the Federal Reserve. It convinced me that the only solution to our economic troubles is the Monetary Reform Act. Before that, I had no idea how to get out of this mess. Why can’t our politicians get this? In a single year America could once again be on the path to political and economic freedom. I hold your work in the highest regard and drew from it heavily for my own film.” Aaron Russo, Feb. 2007, Hollywood Producer, Director and Writer of America, Freedom to Fascism

Russo “I’m a big fan of The Money Masters. It’s undoubtedly the best work on the Federal Reserve. It convinced me that the only solution to our economic troubles is the Monetary Reform Act. Before that, I had no idea how to get out of this mess. Why can’t our politicians get this? In a single year America could once again be on the path to political and economic freedom. I hold your work in the highest regard and drew from it heavily for my own film.” Aaron Russo, Feb. 2007, Hollywood Producer, Director and Writer of America, Freedom to Fascism G Edward Griffin I appreciate and applaud your efforts to accomplish something specific in the area of monetary reform. . . I do not hesitate to recommend that people view The Money Masters for the excellent overview of fraudulent banking which it presents. . . G. Edward Griffin,” author of THE CREATURE FROM JEKYLL ISLAND; A Second Look at the Federal Reserve

G Edward Griffin I appreciate and applaud your efforts to accomplish something specific in the area of monetary reform. . . I do not hesitate to recommend that people view The Money Masters for the excellent overview of fraudulent banking which it presents. . . G. Edward Griffin,” author of THE CREATURE FROM JEKYLL ISLAND; A Second Look at the Federal Reserve W Cleon Skousen “This is undoubtedly the most comprehensive presentation of the history of our money system and who is responsible for the disastrous consequences that has left us with an unconstitutional money system and multi-trillion dollar debt.” – Dr. W. Cleon Skousen, author of The Naked Capitalist and The Naked Communist

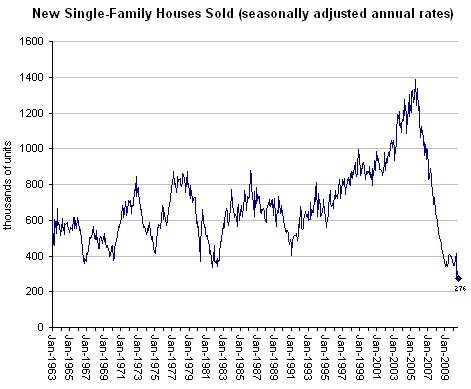

W Cleon Skousen “This is undoubtedly the most comprehensive presentation of the history of our money system and who is responsible for the disastrous consequences that has left us with an unconstitutional money system and multi-trillion dollar debt.” – Dr. W. Cleon Skousen, author of The Naked Capitalist and The Naked Communist Question: What caused the US Housing market collapse? Answer: The Real Causes of the Housing Market Collapse, The National Debt now exceeds $9.2 trillion dollars. In Fiscal Year 2006 the U.S. Government spent $406 billion on interest payments.to holders of that debt. Why do we have such a gigantic debt? Because Democrat and Republican officeholders spend far more than the Government receives in revenue. In 2007 alone, the US government paid out roughly $430 billion in interest to pay for money borrowed to finance previous deficits. The interest total for just the last 20 years – back to 1988 – is well over $6.5 trillion. Interest payments in 2008 alone will again exceed $400 billion. Where on earth will all that money come from? If the government borrowed it all from the credit markets (i.e., sold US Treasury bills, bonds and notes – government IOUs) to raise the money it would dry up all available credit. Interest rates would skyrocket and the economy would collapse. So how does it do this year after year without such dire effects?

Question: What caused the US Housing market collapse? Answer: The Real Causes of the Housing Market Collapse, The National Debt now exceeds $9.2 trillion dollars. In Fiscal Year 2006 the U.S. Government spent $406 billion on interest payments.to holders of that debt. Why do we have such a gigantic debt? Because Democrat and Republican officeholders spend far more than the Government receives in revenue. In 2007 alone, the US government paid out roughly $430 billion in interest to pay for money borrowed to finance previous deficits. The interest total for just the last 20 years – back to 1988 – is well over $6.5 trillion. Interest payments in 2008 alone will again exceed $400 billion. Where on earth will all that money come from? If the government borrowed it all from the credit markets (i.e., sold US Treasury bills, bonds and notes – government IOUs) to raise the money it would dry up all available credit. Interest rates would skyrocket and the economy would collapse. So how does it do this year after year without such dire effects?

Here is the trick. Take, for example, a year like this year in which the government runs a $400 billion dollar deficit. The Treasury Department has to sell $400 billion in US Treasury bills, bonds and notes (government IOUs) to buyers at a rate of interest sufficient to attract their money (and beat the interest competition of other banks’ CDs and other governments’ bills, bonds and notes). To avoid a credit squeeze, the Federal Reserve System Open Market Committee in Washington directs the NY Federal Reserve Bank to purchase roughly 10% of that total (or $40 billion in our example) in existing US bills, bonds, and notes from the current holders. To pay for them it creates the $40 billion out of nothing, merely with keystrokes on a computer. Through more keystrokes, this new $40 billion is deposited into the banks of the various bill, bond, and note sellers, thereby increasing the reserves of those banks by $40 billion.

Pursuant to the Federal Reserve Act of 1913 those banks must keep only 10% of those new deposits on “reserve.” (Because these banks do not have to keep 100% on reserve, this banking system is called a “fractional reserve” system.). So of the $40 billion deposited, the banks must keep 10% on reserve ($4 billion) and may loan out $36 billion (90%), for business loans, mortgages, credit card loans, to purchase government bonds – for whatever borrowers want. Those loans (and payments) are in turn deposited in banks (very few folks put their money in mattresses). So of the $36 billion loaned out and then re-deposited, the banks receiving the new deposits can then loan out 90% or $32.4 billion, retaining 10% or $3.6 billion as reserves.

Banks repeat this redeposit-reloan process, reduced 10% each time, until the 10% reserves retained have reduced the funds available for loan to zero. This cunning process allows the banks to create out of nothing nine times the original $40 billion in new deposits received from the Federal Reserve (the “Fed”), or $360 billion dollars. This total is concealed from the public by the only partial expansion of the loan total at each repetitive step.

Banks repeat this redeposit-reloan process, reduced 10% each time, until the 10% reserves retained have reduced the funds available for loan to zero. This cunning process allows the banks to create out of nothing nine times the original $40 billion in new deposits received from the Federal Reserve (the “Fed”), or $360 billion dollars. This total is concealed from the public by the only partial expansion of the loan total at each repetitive step.

We can easily see that even by the second re-loan step mentioned above, the banks have loaned out $68.4 billion based on the original $40 billion deposited. The end result of the process is that the banks receiving the deposits and re-deposits collectively have loaned out $360 billion dollars, which they created out of nothing, and have retained $40 billion in reserve. The Fed created the first $40 billion, the banks $360 billion, equaling $400 billion dollars. Thus the credit markets are stabilized even though the US government has borrowed $400 billion.

But notice, the Fed only created the initial 10% ($40 billion). Privately owned banks created 90% ($360 billion) out of nothing, and loaned it out at interest. At even 6% that is $21.6 billion dollars per year in interest. Some of this profit goes to the private stockholders of the banks. However, the banks conceal much of this vast profit from the public as undistributed or retained earnings. Five banks hold over 50% of all deposits in the United States. This means that in a year with a $400 billion deficit (such as FY 2007-2008), those five banks will receive over 50% of approximately 6% interest on the newly created $360 billion: over $10 billion per year, from now on, for creating money out of nothing. This is profoundly unjust, and dangerous to any government, especially in a country that prides itself on being a democracy.

Note that the Fed, not the United States Treasury, created the initial $40 billion in our example. The 12 Federal Reserve banks are private corporations the stock of which is owned by private banks in their districts, not by the United States Government. The United States Treasury pays the Fed interest on the US bills, bonds, and notes the Fed buys with the money it creates out of nothing. The Fed routinely holds about 10% of the United States National Debt (US Treasury bills bonds, notes), which it has accumulated to provide the base for the rest, as explained above.

6% interest on the nearly trillion dollars in bonds it now owns provides the Fed with roughly $50 billion in revenue. With this money the Fed (1) pays some money to its private banks stockholders, (2) uses some to create giant unaudited slush funds to manipulate currency and stock markets (ostensibly to help avoid economic crises such as the one we are currently in), and (3) then takes out whatever it wishes – without any Congressional oversight or external audit – for expenses, salaries, perks, jets, lavish parties, etc.. The rest it returns to the US Treasury. In this manner the Federal Reserve operates independently of our elected Congress and external oversight.

A well-meaning, but later-disillusioned President Woodrow Wilson signed into law The Federal Reserve Act of 1913 that authorized this profoundly unjust system. This law transferred money creation from our elected government to private banks. The vast economic wealth that contorted and deliberately complex law of 1913 concentrated in the hands of the privately-owned national banks is almost incalculable. It is concentrating the wealth of the nation in fewer and fewer hands as they create over 90% of our new money, year after year, and receive the interest tribute on it from the American people to whom they have loaned it.

Deficits fuel the fire of economic injustice by requiring borrowing which requires new money creation, by the private banks. Wars fuel deficits. Conflicts and fear fuel wars. The mass media fuels conflicts and fear. The bankers own and/or control the mass media. Full circle.

Apart from the horrific greed of the banks and mortgage companies making the deceptive sub prime loans, the creation of new money to pay for wars and other deficit-spending results in inflation. Too much money at a time with the same amount of goods for sale drives up prices. To combat this the Fed raises interest rates. Higher interest rates hurt the housing market. Repeated and large deficits require repeated interest rate interest hikes to avoid severe inflation. Since Americans were on the edge economically already, the housing market was killed.

Apart from the horrific greed of the banks and mortgage companies making the deceptive sub prime loans, the creation of new money to pay for wars and other deficit-spending results in inflation. Too much money at a time with the same amount of goods for sale drives up prices. To combat this the Fed raises interest rates. Higher interest rates hurt the housing market. Repeated and large deficits require repeated interest rate interest hikes to avoid severe inflation. Since Americans were on the edge economically already, the housing market was killed.

Now that the housing market is dead, can the Fed resurrect it? Perhaps. Certainly lower interest rates and tax breaks (to a much lesser degree) will help. But so many Americans are already bankrupt, or unemployed, or broke, that they simply cannot qualify for or afford any loan, house, or even, increasingly, a rental. They are now homeless, or living in homes owned by the banks, so that most Americans are now debt slaves on the continent their great, great, great, grandfathers conquered. The bankers own it all, or very nearly so. Once the “recession” has been halted – if it can be – the Fed will have to raise interest rates, rather quickly, to avoid severe inflation caused by all the deficits. Again, full circle. Besides the concentration of wealth into fewer and fewer hands it causes, fractional reserve banking is the primary cause of the inherent instability in our economic system and of its boom-bust “cycles.”

Until the American people cease being foolish consumers and realize how the banking system in the United States really works – and fight to reform it – they will remain slaves to the bankers, who will become increasingly harsh taskmasters and injustice and wars will multiply. Soon, very soon, America will consist – like the 3rd world countries – of only the very few very rich and the very many very poor.

Understand now why the banks are the largest buildings in every town in the US?, why the bankers fought tooth and nail to get the Federal Reserve Act of 1913 passed, giving them the power to create the great majority of the US money supply (excepting the tiny fraction in coin issued by the U.S. mint)?, why banks like wars and deficit spending, and why we unfailing have deficits every single year, regardless of which bank puppets they get elected using the mass media they own and control?

Each generation is faced with the same choice. Our forefathers made their choice – to be free. Have we made ours – to be slaves? (copyright 2008)

Question: Who owns the Federal Reserve Banks? Answer: The Federal Reserve Banks of each region are owned by (issue their stock exclusively to) the member banks of that same region. The member banks are privately owned corporations. Thus the Federal Reserve Banks are privately owned. This is a matter of law and anyone may read the Federal Reserve Act of 1913 for themselves (see below).

Question: Why then do some people deny that the Federal Reserve Banks are owned by private corporations? Answer: Three groups of people deny this fact, for differing reasons:

The first group consists of the private owners of the Federal Reserve Banks, and their shills. It is obviously not in their interest that the American people realize that private bankers own what most people regard as a part of the public treasury and government. The people would doubtless not like it if they knew that the stockholders of the Federal Reserve Banks receive 6% interest (raised higher in the past) per year on their stock ownership, risk free. The people would be legitimately concerned to know that the member bank stockholders elect six of the nine members (i.e., 2/3rds) of the Boards of the reserve banks of their regions. Rather than regulating or controlling the activities of private banks in their regions, the opposite is the case.

The second group consists of those persons who, in their ignorance, have believed the propaganda of the Federal Reserve Banks, which sometimes issue ambiguous, doublespeak statements attempting to obfuscate their private bank ownership. Here is a typical example from the NY Fed website, quite easily seen through: Although they are set up like private corporations and member banks hold their stock, the Federal Reserve Banks owe their existence to an act of Congress and have a mandate to serve the public. Therefore, they are not really “private” companies, but rather are “owned” by the citizens of the United States Member banks do, however, receive a fixed 6 percent dividend annually on their stock and elect six of the nine members of the Reserve Bank’s of their region the Reserve Banks issue shares of stock to member banks.

The third group consists of those people who consider that because the Chairman of the Federal Reserve Board of Governors is appointed by the President and approved by the Senate that the Fed is firmly under government control and that this is sufficiently equivalent to ownership to put them at ease (never mind the outright private bank control of the 12 regional Federal Reserve Banks). Let’s hear how the Fed itself regards such indirect government control (again from the NY Fed website): The Federal Reserve System is not “owned” by anyone and is not a private, profit-making institution. Instead, it is an independent entity within the government, having both public purposes and private aspects.

If you are a little uncomfortable with your Fed having private aspects, you are not alone. Notice also the contradiction with the other NY Fed quote above, which claims the citizens of the US own the Fed here it claims no one owns it (same website). The truth and the law is that the member banks own and control all 12 Federal Reserve Banks. Another interesting doublespeak quote from the NY Fed website: Therefore, the Federal Reserve can be more accurately described as “independent within the government. A little independence is a good thing, unless that independence is in reality virtually total and the entity involved controls the nation’s money and economy. Think about it: if the Fed is independent from the government that created it, then who controls it – it has no brain of its own – it is not a person. If it is not controlled by our government, then by whom?

Question: Doesn’t the fact that the President appoints the Board of Governors of the Federal Reserve System make it a quasi-governmental sort of entity? Answer: Yes, but how “quasi” is quasi-enough? The Board of Governors of the System consists of 7 members, one appointed every two years (one term begins every two years, on February 1 of even-numbered years, a full year after inauguration day) by the President and confirmed by the Senate for 14 year terms. Wow -those are really long terms. Why? Let’s see: if a new President comes into office pledged to reform the Fed, end its independence from effective government oversight, throw the rascals out and replace them with his own appointees, he had better be very patient, as he can only replace one member every two years. So in his four year term (10 years less than Fed Governors – terms) he can replace only two of the 7 members. Of course, he had better be able to sustain the ire of the remaining Governors (almost all connected to financial institutions indirectly in various academic and think-tank institutions financed by banks and bank grants or loans, or which they hope to join in revolving door relationships after their single terms are up), who can run the economy up, down or sideways, in the interim.

But assuming the President can sustain the fight with the Fed, its bank-PAC financed cheerleaders in the Senate, voters upset over a suddenly sinking economy, the banks who control the Fed and the media giants they also own, then all this brave but foolhardy President has to do is get elected to a second term, and hang on long enough to appoint two more Board members. Thus, assuming all of this goes well, in the span of seven years (a glacial pace in American politics), near the end of his second term, he can finally begin some reform – if he manages to get his four appointees confirmed, is still in office and has any allies left – even in his own party. We think the prefixed word quasi-governmental is a good one, if you understandquasi- to mean pseudo.

Keep in mind also the distinction between the 12 regional Federal Reserve Banks, and the Federal Reserve System as a whole. The private ownership of the 12 Federal Reserve banks we addressed above. “Federal Reserve System” usually refers to the entire framework established by the Federal Reserve Act of 1913, including those 12, privately owned Federal Reserve Banks, and the Board of Governors of the system, which meets in Washington D.C. The Fed Board of Governors was also established by the Act of 1913. These are the 7 members with 14-year terms, also mentioned above. Two of them are appointed by the President to 4-year terms as Chairman and Vice Chairman of the Board (largely nominal positions – no extra votes). They, of course, are not owned like corporation stock is owned. So when someone is trying to mislead folks by denying any private ownership of the Fed, they will inevitably refer to the Federal Reserve System (rather than to the Federal Reserve Banks) and declare it is not privately owned (which is partly true [the Fed Board of Governors is not “owned”], and partly false [the 12 Federal Reserve banks are]). We have addressed these two elements in detail, above.

United States Note

Question: Have the Courts had to decide whether the Federal Reserve Banks are privately owned or not? Answer: Yes, in several cases. Here is one of them on point which went up to the 9th Circuit Court of Appeals: LEWIS v. UNITED STATES John L. LEWIS, Plaintiff/Appellant v. UNITED STATES of America, Defendant/Appellee. No. 80-5905. United States Court of Appeals, Ninth Circuit. Submitted March 2, 1982; Decided April 19, 1982; As Amended June 24, 1982

“Plaintiff, who was injured by vehicle owned and operated by a federal reserve bank, brought action alleging jurisdiction under the Federal Tort Claims Act. The United States District Court for the Central District of California, David W. Williams, Jr., dismissed holding that federal reserve bank was not a federal agency within meaning of Act and that the court therefore lacked subject-matter jurisdiction. Appeal was taken. The Court of Appeals, Poole, Circuit Judge, held that federal reserve banks are not federal instrumentalities for purposes of the Act, but are independent, privately owned and locally controlled corporations. Affirmed

.. . .Examining the organization and function of the Federal Reserve Banks and applying the relevant factors, we conclude that the Reserve Banks . . . are independent, privately owned and locally controlled corporations.

Each Federal Reserve Bank is a separate corporation owned by commercial banks in its region. The stockholding commercial banks elect two-thirds of each Bank’s nine member board of directors. The remaining three directors are appointed by the Federal Reserve Board. The Federal Reserve Board regulates the Reserve Banks, but direct supervision and control of each Bank is exercised by its board of directors. 12 U.S.C. § 301. The directors enact by-laws regulating the manner of conducting general Bank business, 12 U.S.C. § 341, and appoint officers to implement and supervise daily Bank activities. These activities include collecting and clearing checks, making advances to private and commercial entities, holding reserves for members banks, discounting the notes of members banks, and buying and selling securities on the open market. See 12 U.S.C. §§ 341-361.

. . . The Banks are listed as neither “wholly owned” government corporations under 31 U.S.C. § 846 nor as “mixed ownership” corporations under 31 U.S.C. § 856, . . .

Additionally, Reserve Banks, as privately owned entities, receive no appropriated funds . . .”

Let’s sum up: The Federal Reserve consists of 12 regional banks, the stock of which is owned and the Boards controlled by the member banks, which are privately owned bank corporations. These institutions receive 6% profit on their funds paid into the Fed, rain or shine, peace or war (sometimes more).

The Federal Reserve Board of Governors is an independent (its own word) entity “within” the government (i.e., something much like an independent, internal parasite in a host organism), with 14 year, reform-proof terms (i.e., only one of 7 can be replaced every two years).

The Fed was deliberately designed to appear as a sort of government body to hide the fact that it is a private banking cartel whose member banks share in the vast profits of seigniorage (i.e., the difference between the cost of printing/minting or otherwise creating money [a few cents per $100], and its face value). Yes, the Department of the Treasury does still mint our coins (at the US mint) but that represents under 1% of the US money supply, the great bulk of which is simply bankbook entries – electronic keyboard impulses in computer memories – created by banks on-the-spot to fund loans they make in response to loans applications their “customers” submit (hence the competition by banks for your loan applications and credit card borrowing).

Wouldn’t you love to have that exclusive ability – simply to type numbers on your keyboard creating bank accounts, and then write checks or charge purchases to those accounts (actually, no – it is gravely unjust to everyone else and is impoverishing the world for that power to be in private hands).

The Federal Reserve Notes we all accept as currency (there are no U.S. Notes printed since passage of the ill-advised, 1994 Reigle Act abolished Lincoln’s greenbacks) are actually sold to the Fed at the cost of printing – a few cents per sheet – by the Treasury Department Bureau of Engraving and Printing. Seignior age is properly a benefit solely to government (and indirectly then to the people) – not to private bankers – that the Federal Reserve Act, passed by misrepresentation and deception, transferred to the bankers. Thus, rather than the government receiving the vast benefits of creating all of our money, private banks create over 98% of our money supply – literally billions of dollars annually – and pocket the interest charged on loaning that new money, as their private profit. Our government is left with only the insignificant seignior age from minting coins.

Since the bankers actually wanted to control the new, national central bank (called the Federal Reserve Banks), to accomplish this they had to make it appear governmental, which accounts for the occasional use of the term quasi-governmental, to describe this governmental facade. This also explains the construction of the Federal Reserve headquarters building on the Mall in Washington, DC, right in the midst of the authentically governmental buildings there.

The real problem is, thus, not the Fed itself (it only makes about 2% of the money supply – the base for the rest), it’s the private banks that, pursuant to the fractional reserve banking authorized by the Federal Reserve Act of 1913, make/create-from-nothing-for-their-private-profit the other roughly 98% of the US money supply. The Fed is just a quasi-governmental smokescreen (and central organizing body) for the private banking cartel’s money-creation operation.

But don’t believe the above on our word alone, read it for yourself:

[Note: Additional FAQ and Answers follow these Federal Reserve Act excerpts.]

FEDERAL RESERVE ACT SECTION 5: Stock Issues; Increase and Decrease of Capital 1. Amount of Shares; Increase and Decrease of Capital; Surrender and Cancellation of Stock

The capital stock of each Federal reserve bank shall be divided into shares of $100 each. The outstanding capital stock shall be increased from time to time as member banks increase their capital stock and surplus or as additional banks become members, and may be decreased as member banks reduce their capital stock or surplus or cease to be members. Shares of the capital stock of Federal reserve banks owned by member banks shall not be transferred or hypothecated. When a member bank increases its capital stock or surplus, it shall thereupon subscribe for an additional amount of capital stock of the Federal reserve bank of its district equal to 6 per centum of the said increase, one-half of said subscription to be paid in the manner hereinbefore provided for original subscription, and one-half subject to call of the Board of Governors of the Federal Reserve System. A bank applying for stock in a Federal reserve bank at any time after the organization thereof must subscribe for an amount of the capital stock of the Federal reserve bank equal to 6 per centum of the paid-up capital stock and surplus of said applicant bank, paying therefore its par value plus one-half of 1 per centum a month from the period of the last dividend. When a member bank reduces its capital stock or surplus it shall surrender a proportionate amount of its holdings in the capital stock of said Federal Reserve bank. Any member bank which holds capital stock of a Federal Reserve bank in excess of the amount required on the basis of 6 per centum of its paid-up capital stock and surplus shall surrender such excess stock. When a member bank voluntarily liquidates it shall surrender all of its holdings of the capital stock of said Federal Reserve bank and be released from its stock subscription not previously called. In any such case the shares surrendered shall be canceled and the member bank shall receive in payment therefore, under regulations to be prescribed by the Board of Governors of the Federal Reserve System, a sum equal to its cash-paid subscriptions on the shares surrendered and one-half of 1 per centum a month from the period of the last dividend, not to exceed the book value thereof, less any liability of such member bank to the Federal Reserve bank.

SECTION 10: Board of Governors of the Federal Reserve System1. Appointment and Qualification of Members

The Board of Governors of the Federal Reserve System (hereinafter referred to as the “Board”) shall be composed of seven members, to be appointed by the President, by and with the advice and consent of the Senate, after the date of enactment of the Banking Act of 1935, for terms of fourteen years except as hereinafter provided, but each appointive member of the Federal Reserve Board in office on such date shall continue to serve as a member of the Board until February 1, 1936, and the Secretary of the Treasury and the Comptroller of the Currency shall continue to serve as members of the Board until February 1, 1936. In selecting the members of the Board, not more than one of whom shall be selected from any one Federal Reserve district, the President shall have due regard to a fair representation of the financial, agricultural, industrial, and commercial interests, and geographical divisions of the country. The members of the Board shall devote their entire time to the business of the Board and shall each receive an annual salary of $15,000, payable monthly, together with actual necessary traveling expenses.

Prior to the enactment of the Banking Act of 1935, approved Aug. 23, 1935, the Board of Governors of the Federal Reserve System was known as the Federal Reserve Board. See note to the third paragraph of section 1. The portion of this paragraph dealing with salaries of Board members has in effect been amended numerous times, most recently by Executive Order. Prior to the act of December 27, 2000, section 1002 of which revised the executive schedule, the salary of the chairman of the Board was set at executive schedule level 2 and the salary of other members at level 3. The salary of the chairman of the Board is now set at executive schedule level I, and the salary of other members at level II (see 2 USC 358 and 5 USC 5313 and 5314).]

SECTION 19: Bank Reserves

[(2)(A)(i&ii) below, authorizes fractional reserve banking]

Reserve Requirements

(2) Reserve requirements.

(A) Each depository institution shall maintain reserves against its transaction accounts as the Board may prescribe by regulation solely for the purpose of implementing monetary policy;

(i) in the ratio of 3 per centum for that portion of its total transaction accounts of $25,000,000 or less, subject to subparagraph (C); and (ii) in the ratio of 12 per centum, or in such other ratio as the Board may prescribe not greater than 14 per centum and not less than 8 per centum, for that portion of its total transaction accounts in excess of $25,000,000, subject to subparagraph (C). [MM Note: this section authorizes banks to make loans while retaining only 8-14% reserves (it is presently set by the Fed Board at 10% for most types of loans). This is the legal authority for fractional reserve banking. The result is that private banks (not the government) create over 90% of the US money supply. A proper reform, as detailed in the Money Masters video, would raise this to 100%, providing the necessary liquidity to do so by retiring the national debt with US Notes.]

(B) Each depository institution shall maintain reserves against its non personal time deposits in the ratio of 3 per centum, or in such other ratio not greater than 9 per centum and not less than zero per centum as the Board may prescribe by regulation solely for the purpose of implementing monetary policy.

(D) Any reserve requirement imposed under this subsection shall be uniformly applied to all transaction accounts at all depository institutions. Reserve requirements imposed under this subsection shall be uniformly applied to non personal time deposits at all depository institutions, except that such requirements may vary by the maturity of such deposits.

(6) Exemption for certain deposits. The requirements imposed under paragraph (2) shall not apply to deposits payable only outside the States of the United States and the District of Columbia, except that nothing in this subsection limits the authority of the Board to impose conditions and requirements on member banks under section 25 of this Act or the authority of the Board under section 7 of the International Banking Act of 1978 (12 U.S.C. 3105).

Question: How does the Fed “create” money out of nothing? Answer: It is a four-step process. But first a word on bonds. Bonds are simply promises to pay — or government IOUs. People buy bonds to get a secure rate of interest. At the end of the term of the bond, the government repays the principal, plus interest (if not paid periodically), and the bond is destroyed. There are trillions of dollars worth of these bonds at present. Now here is the Fed moneymaking process:

Step 1. The Fed Open Market Committee approves the purchase of U.S. Bonds on the open market.

Step 2. The bonds are purchased by the New York Fed Bank from whomever is offering them for sale on the open market.

Step 3. The Fed pays for the bonds with electronic credits to the seller’s bank, which in turn credits the seller’s bank account. These credits are based on nothing tangible. The Fed just creates them.

Step 4. The banks use these deposits as reserves. Most banks may loan out ten times (10x) the amount of their reserves to new borrowers, all at interest.

In this way, a Fed purchase of, say a million dollars worth of bonds, gets turned into over 10 million dollars in bank deposits. The Fed, in effect, creates 10% of this totally new money and the banks create the other 90%.

This also explains why the Fed consistently holds about 10% of the total US Treasury bonds. It had to buy those (with accounts or Fed notes the Fed simply created) from the public in order to provide the base for the rest of the money the private banks then get to create, most of which eventually winds up being used to purchase Treasury bonds, thus supplying Congress with the borrowed money to pay for its expenditures.

Due to a number of important exceptions to the 10% reserve ratio, some loans require less than 10% reserves, and many no (0%) reserves, making it possible for banks to create many times more than ten times the money they have in “reserve”. Due to these exceptions from the 10% reserve requirement, the Fed creates only a little under 2% of the total US money supply, while private banks create the other 98%.

To reduce the amount of money in the economy, the process is just reversed — the Fed sells bonds to the public, and money flows out of the purchaser’s local bank. Loans must be reduced by ten times the amount of the sale. So a Fed sale of a million dollars in bonds, results in 10 million dollars less money in the economy.

Question: If private banks create over 90% of the US money supply, then are they not a greater threat to our democracy than the Fed itself? Answer: Of course. The Fed was simply a smoke-screen designed to hide the stark reality that behind the Federal Reserve Act of 1913, signed by an unwitting President Wilson (who later deeply regretted that act) was a monumental power grab by the largest bankers who designed the Act at their secret meeting at Jekyll Island, Georgia (detailed in the video/DVD). The Federal Reserve Act allowed the Fed to establish a reserve requirement of between only 8% and 14% (presently set at 10% for most types of loans). That made it lawful for banks to loan far more than they had in deposits – to practice fractional reserve banking. The Fed centralized, nationalized and standardized this fraud on the people, and restricted its practice to banks only. In fact, the roughly 2% of the US money supply the Fed creates actually is owned by the government (as it should be), but this tiny fraction obscures the fact that it is the base for the creation of the other 98% created by private banks as loans. Thus, simply having a Federal Reserve or similar national Central Bank, in itself, is not a bad thing (it can be a good thing) – but allowing private banks to practice fractional reserve banking (pursuant to the Federal Reserve Act of 1913 or any other such law) is the real problem, which is impoverishing all Americans and now all peoples worldwide, except the bankers. For clarity, it should be renamed the Fractional Reserve Banking Act. The exponential concentration of wealth, in the US and abroad, is due almost exclusively to fractional reserve banking by privately owned banks such as Bank of America, Wells Fargo, Citigroup, J.P. Morgan Chase, etc. The Fed is simply part of the mechanism screening this grave injustice from public knowledge and scrutiny.

Question: If private banks create over 90% of the US money supply, then are they not a greater threat to our democracy than the Fed itself? Answer: Of course. The Fed was simply a smoke-screen designed to hide the stark reality that behind the Federal Reserve Act of 1913, signed by an unwitting President Wilson (who later deeply regretted that act) was a monumental power grab by the largest bankers who designed the Act at their secret meeting at Jekyll Island, Georgia (detailed in the video/DVD). The Federal Reserve Act allowed the Fed to establish a reserve requirement of between only 8% and 14% (presently set at 10% for most types of loans). That made it lawful for banks to loan far more than they had in deposits – to practice fractional reserve banking. The Fed centralized, nationalized and standardized this fraud on the people, and restricted its practice to banks only. In fact, the roughly 2% of the US money supply the Fed creates actually is owned by the government (as it should be), but this tiny fraction obscures the fact that it is the base for the creation of the other 98% created by private banks as loans. Thus, simply having a Federal Reserve or similar national Central Bank, in itself, is not a bad thing (it can be a good thing) – but allowing private banks to practice fractional reserve banking (pursuant to the Federal Reserve Act of 1913 or any other such law) is the real problem, which is impoverishing all Americans and now all peoples worldwide, except the bankers. For clarity, it should be renamed the Fractional Reserve Banking Act. The exponential concentration of wealth, in the US and abroad, is due almost exclusively to fractional reserve banking by privately owned banks such as Bank of America, Wells Fargo, Citigroup, J.P. Morgan Chase, etc. The Fed is simply part of the mechanism screening this grave injustice from public knowledge and scrutiny.

Question: How do private banks create money? Answer: Focusing on the majority of the US money supply, the method is as follows: The Federal Reserve Notes and equivalent Federal Reserve Deposits (mentioned above) are deposited in local banks or to their credit at one of the 12 Fed banks. These funds serve as the base of bank loans, which require a 10% reserve. For example, if $1,000,000 of Federal Reserve notes or Fed deposits are entered on the books with the Fed to the credit of a bank (usually the bank of the person or company which just sold the Fed a Treasury bond/bill or note), that bank may loan all of that money out (at interest), except for 10% which is kept as its reserve. Thus $900,000 in this example may be loaned out by that bank.

In the usual case, the borrower of the $900,000 will not, of course, keep the money under the mattress, rather, it is deposited either in the same bank or in others. This $900,000 in new deposits may then be loaned out at interest by these banks, except for the 10% reserve. Thus $810,000 is loaned out a second time ($90,000 of the $900,000 being retained as reserves).

The newly loaned $810,000 is then deposited in these or other banks, allowing them to lend out $729,000 a third time (retaining 10% = $81,000 as reserves), and so on. This process gets repeated over and over, each time the lending bank(s) retains 10%. It takes a series of 66 loans to reduce the funds available for relending to less than $1,000 by retention of 10% each time as bank reserves. In actual practice, due to numerous exceptions to the 10% reserve requirement, banks may lend the money even more times, resulting in even more money being created by them.

Thus, in our example, an original purchase by the Fed of $1,000,000 in Treasury bonds on the open market, by a series of deposits and loans in one or more banks, results in an expansion of the US money supply (via bank accounts simply created as loans by the lending banks) by a factor of 10x. After the process is completed, the total money in the US economy has been expanded by ten million dollars ($10,000,000), in this example. The Fed got to create 10% of this total, and private banks the other 90%, to lend at interest. In each individual bond purchase by the Fed, not just one bank profits from this scheme, rather the banking system as a whole does. However, in practice, the 4 largest international banks get roughly 80% of the profit, leaving the crumbs (still million$) to the smaller banks in your community.

What did the banks do to obtain this right to lend, relend, and relend again and again the same money (less 10% reserved each time)? Nothing, except lobby and mislead the public, the majority of Congress and President Wilson to think they were supporting legislation to reform banking to a more just form under the Federal Reserve Act of 1913. They continue to hide, obfuscate and mislead the public, to the same purpose, using media they purchased for this purpose, and corrupting the political system in the process.

This critically important piece of legislation – the Federal Reserve Act of 1913 – had to be disguised to accomplish the bankers’ scheme, and so it was. That story is contained in the video/DVD, The Money Masters. For more detailed information (prepared and freely distributed by the Federal Reserve Bank of Chicago but now out of print) we recommend readers read Modern Money Mechanics.